Your accountant wants to help you file your taxes, but they need your help to make the process go as smoothly as possible.

This is why it’s a great idea to make yourself into a client that your accountant loves to see. Not only will you help lower your accountant’s stress levels by being a model client, but you’ll make your own tax season easier and less personally stressful.

So what can you do to make sure your accountant is always happy to see you? Here are the steps you can take to become their favorite client:

Make Sure You Have the Right Accountant

You’ll need to make sure that your accountant is someone who can help you with the specific tax issues you face.

Start with an understanding of the certifications you may encounter. To be a Certified Public Accountant, or CPA, your accountant must have met the educational requirements, passed the Uniform CPA Examination, and met your state’s licensing requirements. An Enrolled Agent, or EA, is a tax practitioner who is federally licensed to represent taxpayers before the IRS. CPAs, EAs and tax attorneys are all authorized to practice in front of the IRS, meaning they can help you handle audits or negotiate with tax collectors on your behalf.

Even with the proper training and licensing, not every CPA or EA will be the right accountant for you. Ask if your accountant is familiar with the specific tax issues that apply to your situation. For instance, if you’re a snowbird who spends the winter in another state, you will want to make sure your accountant is comfortable handling the tax requirements for both of your states of residence.

Get Organized

We all know the cliché of the taxpayer who shows up to their accountant’s office on April 14 with a shoebox full of crumpled receipts and tax documents. Being that client is sure to send your accountant heading for the hills.

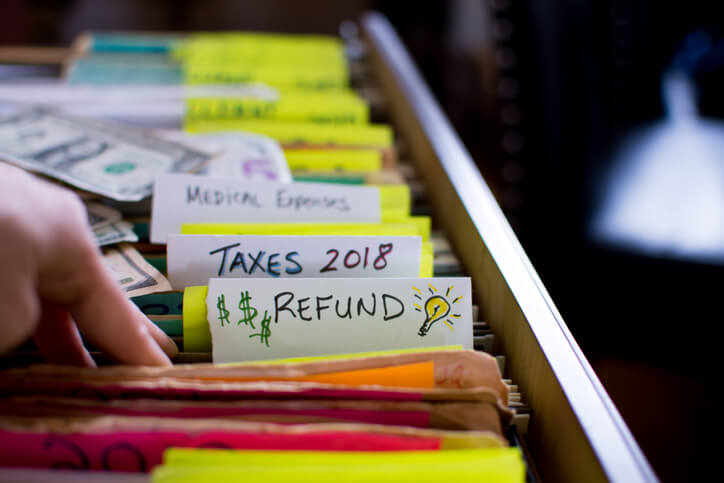

Luckily, the same thing that will make your tax preparation easier will also lower your accountant’s blood pressure: a simple organizational system.

For most taxpayers, a three-folder system will suffice. Create one folder for each of these categories:

- Income

- Expenses

- Deductions

- Investments

1

Income Folder

Whether you are still working and drawing a paycheck or retired and living off of your investments, you will have income statements to bring to your accountant when it’s time to prepare your taxes. Having a folder to collect this information will help you keep track of every penny. In addition, adding a cover sheet where you manually record what you earn as it comes in can help you check the accuracy of official documents, such as Social Security and pension statements.

2

Expenses and Deductions Folder

This will replace your shoebox of disorganized receipts. Start by creating separate files within this folder to represent each category of expenses or deductions, such as business, charitable donations, childcare and medical expenses. Doing this kind of organization of your receipts will help ensure that you don’t miss any necessary receipts. It will help you avoid those head-scratchers when you can’t remember why you saved a specific receipt.

3

Investments Folder

This will be where you save annual statements from your investments, distribution records, notices of dividends and capital gains and losses, and records proving tax-deductible contributions to retirement accounts.

Come Prepared

If you’re not already organized when tax season rolls around — and even the most methodical among us has found papers that aren’t in their proper home — then do not expect your accountant to do your organizing for you. Make sure you come to your meeting with your information as well organized as you can get it.

Remember that your accountant is a tax code expert, not a professional organizer.

As you review the three folders described above, you’ll want to identify the taxes you’ve paid throughout the year, whether that’s in the form of regular deductions, quarterly or estimated payments, or real estate and property tax payments. (And bring copies of last year’s federal and state tax returns for reference, as needed.)

Know What Tax Issues May Affect You

Your accountant does not expect you to know every deduction and tax strategy that could apply to you. However, if you are unaware of how your overall life circumstances may affect your tax liability, it’s tough for your accountant to help you find the best strategies for your situation.

You and Your Accountant: A Love Story

Treating your accountant as a partner in your tax preparation rather than as the person you hire to “deal with it” will go a long way toward making you a favorite client and reducing your own tax season stress.

By doing your homework before you meet, you’ll be better prepared to answer questions and fill in any information gaps that your accountant needs to complete your taxes accurately.

And remember: The right accounting and tax professional can be a personal and financial resource to you all through the year, not only at tax time.